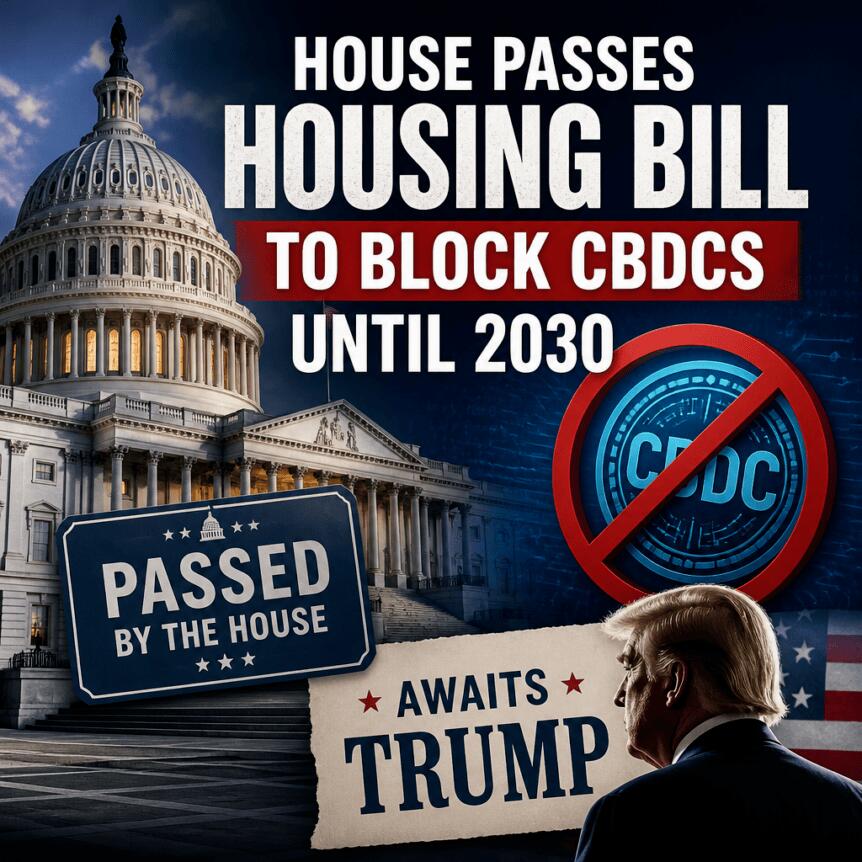

The U.S. House of Representatives has approved sweeping housing legislation that also contains a temporary prohibition on central bank digital currencies (CBDCs), delivering a significant policy victory for lawmakers who have sought to limit central-bank involvement in tokenized money. The measure now moves to President Donald Trump, who is expected to sign the bill into law.

According to the official House roll call, the chamber passed the 21st Century ROAD to Housing Act by a wide margin of 358–32 on Tuesday, following a similarly large vote in the Senate the day before. The bill is designed primarily to address housing affordability, but its CBDC provision—and its stablecoin carve-out—has become the most closely monitored part for the crypto and financial-services sector.

Key takeaways

- The House passed the 21st Century ROAD to Housing Act, with a CBDC restriction aimed at preventing the Federal Reserve from issuing or creating a CBDC or substantially similar digital asset until Dec. 31, 2030.

- The ban is not absolute across all crypto activity: the legislation includes a carve-out for certain dollar-denominated stablecoins described as open, permissionless, and private.

- Congressional leaders reached agreement on the bill only after earlier disagreements, indicating that the CBDC language remained a negotiable but preserved feature.

- The legislation now goes to the president for final approval, potentially shaping how financial institutions and crypto firms prepare for compliance over the 2020s.

What the bill does: a time-limited CBDC prohibition

The CBDC clause included in the housing act would bar the Federal Reserve from, “directly or indirectly,” issuing or creating a central bank digital currency—or any digital asset “substantially similar” to a CBDC—until Dec. 31, 2030. While the language is time-bound, it is intended to constrain central-bank experimentation or deployment of a tokenized central-bank form of money during the remainder of the decade.

In practice, such a restriction can influence institutional planning in several ways. Banks and other regulated financial intermediaries typically rely on clear regulatory signals for product development and risk management. By limiting the Federal Reserve’s ability to pursue a CBDC initiative through direct issuance or creation, the statute aims to reduce uncertainty for firms that view CBDCs as a shift toward centrally controlled settlement rails.

At the same time, the clause’s “substantially similar” formulation may raise interpretive questions about what qualifies as prohibited activity. Institutions subject to supervision may need to evaluate not only explicit CBDC proposals, but also any related digital-asset products that could arguably be characterized as CBDC-like. That creates compliance demand even without a CBDC being launched.

Stablecoin carve-out: narrowing the scope of the restriction

The act also incorporates a carve-out for crypto stablecoins, permitting “dollar-denominated currency” that is described as open, permissionless, and private. This drafting choice signals a legislative intent to avoid an outright ban on stablecoin functionality while still constraining the central-bank issuance of a tokenized form of fiat.

From a policy perspective, the carve-out may be read as an attempt to separate the stablecoin market—particularly private-sector dollar-linked tokens—from central-bank-issued digital currencies. For compliance teams, this distinction matters because it suggests that the bill focuses on the Federal Reserve’s role rather than imposing a blanket prohibition on stablecoin issuance or use.

However, the carve-out’s descriptors—open, permissionless, and private—could require further interpretation depending on how regulators treat access, governance, and transaction privacy. Regulated firms generally maintain compliance controls around transparency, recordkeeping, and supervisory reporting; “private” systems may require additional legal and operational review to ensure they do not undermine auditability or AML obligations.

Legislative momentum and the path to law

The bill’s rapid movement reflects a last-minute agreement among House and Senate leadership on the broader housing measure. According to reporting by Cointelegraph, the House passage followed a prior Senate vote, with the CBDC language carried through negotiations and preserved from earlier versions.

Senate Banking Committee Chairman Tim Scott praised the outcome, framing it as a victory for families while emphasizing that Congress had delivered on a long-standing policy objective. The inclusion of the CBDC prohibition has been repeatedly pursued by Republican lawmakers for years, including through earlier legislation that did not advance to enactment.

One notable precursor was a CBDC-focused proposal from Representative Tom Emmer, the Anti-CBDC Surveillance State Act, introduced in June 2025 and passed by the House in July. Despite clearing the House, it did not move forward in the Senate. The housing bill therefore represents a different legislative route—embedding the CBDC restriction within a must-pass or priority bill—suggesting lawmakers may be using vehicle legislation to achieve digital-asset policy goals when standalone bills stall.

Broader compliance and regulatory implications

For regulated entities, the immediate compliance relevance is the signal the statute sends about congressional boundaries around central-bank digital money. Although the restriction targets the Federal Reserve directly, its presence can affect how other regulators interpret the policy environment in which they supervise payments, tokenized assets, and stablecoins.

Institutions also face a multi-jurisdiction landscape. While the U.S. action is domestic, firms with global operations must continue planning for foreign frameworks such as the EU’s Markets in Crypto-Assets (MiCA) regime. Differences in approach—particularly around token classification, issuer obligations, and stablecoin rules—mean the U.S. CBDC ban may not harmonize with European requirements for reserve management, authorization, and ongoing disclosures.

On enforcement and risk, the bill does not replace existing AML/KYC expectations or consumer-protection rules for crypto and financial intermediaries. Rather, it modifies one dimension of the policy map: the ability of the Federal Reserve to issue or create a CBDC-like digital asset. Compliance programs must therefore remain focused on counterparty due diligence, transaction monitoring, sanctions screening, and recordkeeping, while also tracking whether any new regulatory guidance emerges to clarify how “substantially similar” assets will be treated.

What to watch next

The measure’s next milestone is presidential approval. After the bill becomes law, market participants and supervised entities will likely focus on interpretive clarity around the “substantially similar” standard and the stablecoin carve-out descriptors, as well as any downstream guidance from regulators. The longer-term uncertainty is how these constraints interact with future legislative efforts in U.S. crypto market structure—areas where Congress is still debating rules for trading, custody, and market conduct.

https://www.cryptobreaking.com/house-passes-housing-bill-to/?utm_source=blogger%20&utm_medium=social_auto&utm_campaign=House%20Passes%20Housing%20Bill%20to%20Block%20CBDCs%20Until%202030,%20Awaits%20Trump%20

Comments

Post a Comment